Every month, millions of Americans face a tough choice: pay for their medication or pay for rent. The cost of prescriptions isn’t just high-it’s unpredictable. A pill that costs $5 one month might jump to $500 the next, and no one seems to know why. The truth? You’re caught in the middle of a system designed to obscure prices, not lower them. But you’re not powerless. Understanding how medication costs work-through coupons, generics, and prior authorizations-can save you hundreds, even thousands, a year.

Why Are Prescription Drugs So Expensive in the U.S.?

The U.S. pays more for prescription drugs than any other country. A 30-day supply of insulin might cost $150 here but under $10 in Canada. Why? It’s not about manufacturing. It’s about pricing power. Pharmaceutical companies set list prices, and Pharmacy Benefit Managers (PBMs) negotiate rebates behind closed doors. What you see at the pharmacy counter? That’s the list price-often inflated to make rebates look bigger. The actual cost to the insurer? Sometimes half-or less.

In 2026, the first 10 drugs negotiated under the Inflation Reduction Act (IRA) took effect. These are drugs like Farxiga, Jardiance, and Synjardy. For Medicare beneficiaries, their out-of-pocket cost dropped by an average of 40%. That’s $400 saved per person, per year. But if you’re not on Medicare, you’re still paying full list price unless you find a workaround.

Generic Drugs: The Quiet Hero of Affordable Medication

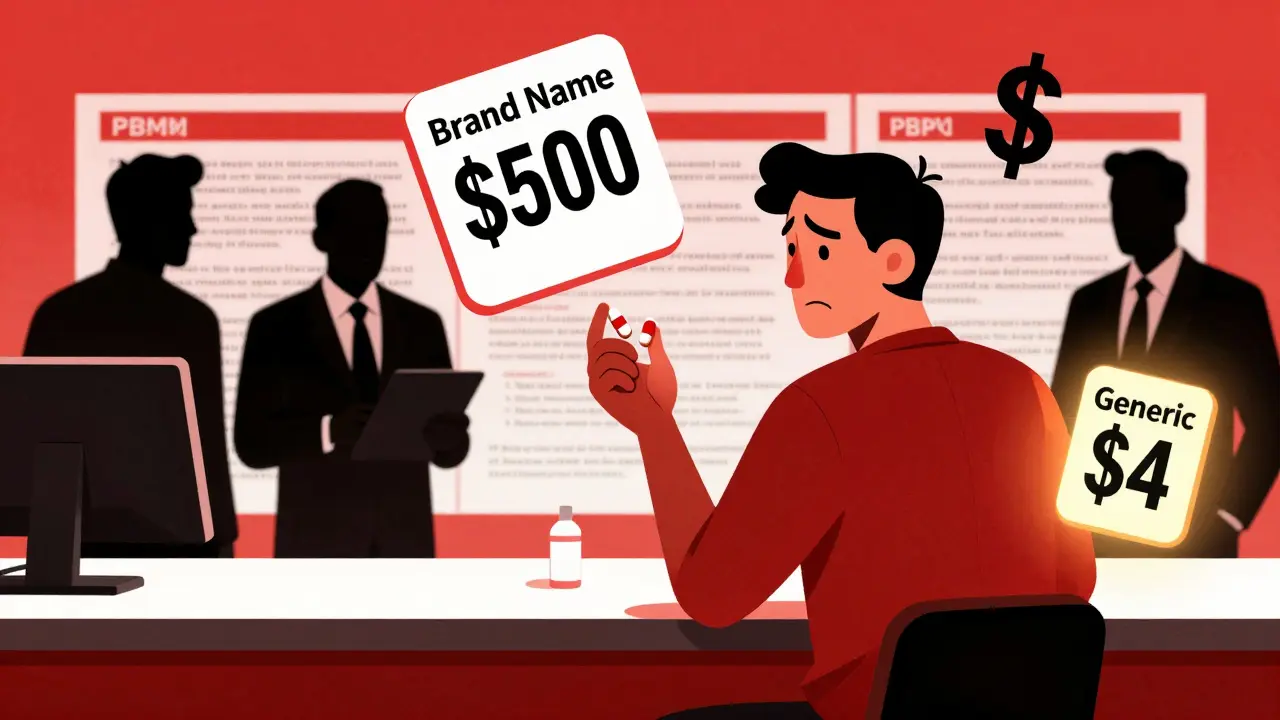

Generic drugs are not cheaper because they’re lower quality. They’re cheaper because they don’t need to recoup billions in R&D. Once a brand-name drug’s patent expires, other manufacturers can produce the same active ingredient. The FDA requires generics to be identical in dosage, strength, safety, and effectiveness. That’s it.

Take lisinopril, a blood pressure pill. The brand version, Prinivil, costs around $120 for a 30-day supply. The generic? $4. That’s 97% less. Same pill. Same effect. Same side effects. But most people don’t ask for it. Their doctor writes the brand. Their pharmacist fills it. And they pay more.

Switching to generics isn’t always automatic. Some doctors still default to brand names. Always ask: "Is there a generic?" If the answer is no, ask why. Sometimes it’s habit. Sometimes it’s marketing. Rarely is it medical necessity.

Prescription Coupons: Helpful-or a Trap?

Coupons look like a gift. "Save $50 on your next prescription!" But here’s what they don’t tell you: coupons often only work for brand-name drugs. And they’re paid for by the drug company-not the insurer. That means you’re still paying the inflated list price, and the coupon just makes it feel affordable.

Worse? Some coupons prevent you from using your insurance. If you use a coupon, your pharmacy might not count the payment toward your deductible or out-of-pocket maximum. That means you’re spending money that doesn’t help you reach your cap. Next year, you’ll be right back where you started.

There’s one good use for coupons: if you’re uninsured or underinsured and have no other option. But always compare the coupon price to the cash price at your pharmacy. Sometimes, the cash price is lower-even without a coupon. Use GoodRx or SingleCare to check real-time prices before you pay.

Prior Authorization: The Bureaucratic Gatekeeper

Prior authorization is when your insurance says: "Wait. We need to approve this drug before you get it." It sounds simple. It’s not. Your doctor fills out paperwork. You wait days-or weeks. Sometimes, they deny it. Then you appeal. And sometimes, you still don’t get the drug.

Why does this happen? Insurance companies use prior authorization to push you toward cheaper alternatives. They might require you to try a generic first. Or a different brand. Or even a non-drug treatment. It’s not always about cost-it’s about control.

But here’s the catch: prior authorization doesn’t always save money. It delays care. And delays can lead to worse health outcomes. A patient with diabetes who can’t get their GLP-1 medication for six weeks might end up in the ER. The hospital bill? Ten times what the drug would’ve cost.

If your prior authorization is denied, don’t give up. Ask your doctor to write a letter of medical necessity. Include lab results, past treatment failures, and side effects. Some insurers have faster appeals for urgent cases. Call your plan and ask: "What’s the process for an expedited appeal?"

How the New Medicare Rules Are Changing the Game

Starting in January 2026, Medicare Part D has three big changes:

- A $2,000 annual out-of-pocket cap on drug costs-no more unlimited spending.

- The "donut hole" coverage gap is gone. You won’t hit a wall where you pay 100%.

- The first 10 negotiated drugs are now priced lower-sometimes half what they were.

That’s huge. Nearly 19 million Medicare beneficiaries will save an average of $400 a year. But here’s the thing: these savings don’t automatically extend to private insurance. If you’re under 65 and on a commercial plan, you’re still stuck with the old system.

Some states are stepping in. Minnesota now uses the Medicare negotiated prices as a cap for Medicaid and commercial plans. Other states are watching. If this works, it could become a national model.

What You Can Do Right Now to Lower Your Costs

You don’t need to wait for policy changes. Here’s what works today:

- Ask for the generic. Always. Even if your doctor says "it’s better." Ask for proof.

- Compare cash prices. Use GoodRx, SingleCare, or RxSaver. Prices vary wildly-even between pharmacies on the same street.

- Ask about 340B pharmacies. If you’re low-income or on Medicaid, some clinics and hospitals sell drugs at 340B discounted rates. Call your local community health center.

- Split pills (if safe). Some pills can be safely split in half. Ask your pharmacist. A $100 pill might cost $50 if you take half.

- Apply for patient assistance programs. Most drugmakers offer free or low-cost meds to people who qualify. Go to NeedyMeds.org. It’s free, and it works.

- Don’t skip doses to save money. That’s dangerous. Instead, call your doctor. They might switch you to a cheaper alternative.

The Bigger Picture: Why This Matters Beyond Your Wallet

Medication costs aren’t just about money. They’re about health. People skip pills because they can’t afford them. One study found that nearly 1 in 4 Americans don’t fill prescriptions due to cost. That leads to more hospitalizations, more ER visits, and more deaths.

When you fight for lower drug prices, you’re not just saving cash-you’re saving lives. The system is broken. But change is happening. The IRA is the biggest shift in drug pricing since Medicare Part D started in 2003. And it’s only getting started.

Next year, 15 more drugs will be eligible for Medicare negotiation. Then 20. Then 30. Each one brings down prices for millions. And if states follow Minnesota’s lead, those savings could spread to private insurance too.

You’re not just a patient. You’re a consumer. And you have more power than you think.

Are generic drugs really as effective as brand-name drugs?

Yes. The FDA requires generics to have the same active ingredient, strength, dosage form, and route of administration as the brand-name version. They must also meet the same strict standards for purity, stability, and performance. Studies show generics work just as well. The only differences are in inactive ingredients like color or filler-things that don’t affect how the drug works in your body.

Why does my prescription cost more at one pharmacy than another?

Pharmacies negotiate different prices with Pharmacy Benefit Managers (PBMs). Some pharmacies get better deals, especially if they’re part of a large chain or have a contract with a specific insurer. Cash prices can also vary widely because PBMs don’t control them. Always check multiple pharmacies. A local independent pharmacy might offer a better price than a big chain.

Can I use a coupon and my insurance together?

Usually not. Most coupons are designed to be used instead of insurance. If you use a coupon, your payment won’t count toward your deductible or out-of-pocket maximum. That means you’re paying more over time. Only use a coupon if the cash price with the coupon is lower than your insurance copay-and you’re okay with not counting it toward your cap.

What should I do if my prior authorization is denied?

Don’t accept the denial. Ask your doctor to submit a letter of medical necessity with clinical evidence-lab results, previous treatment failures, side effects. You can also call your insurance company to request an expedited appeal if your condition is urgent. Many insurers have a 72-hour turnaround for urgent cases. Keep records of every call, email, and form you submit.

Is there help for people who can’t afford their meds even with generics and coupons?

Yes. Most drug manufacturers offer patient assistance programs for low-income individuals. Programs like NeedyMeds, RxAssist, and the Partnership for Prescription Assistance can connect you to free or deeply discounted medications. You’ll need to provide income proof, but the process is straightforward. Some nonprofit pharmacies also offer medications at 340B prices if you qualify.

Will the new Medicare drug price negotiations affect people under 65?

Not directly. But they might indirectly. States like Minnesota are already using Medicare’s negotiated prices as a cap for Medicaid and commercial plans. If more states follow, private insurers could be pressured to lower prices too. It’s not guaranteed, but it’s happening-and it’s the most promising path to broader savings.

Next Steps: What to Do Today

Don’t wait for the system to fix itself. Take action now:

- Review your next prescription. Is it brand or generic? Ask for the generic.

- Check the cash price with GoodRx before you fill it.

- If you’re on Medicare, check if your drug is one of the 10 newly negotiated ones.

- If you’re denied a drug through prior authorization, start your appeal immediately.

- Visit NeedyMeds.org. It takes 10 minutes. It could save you $1,000 a year.

Medication shouldn’t be a luxury. It’s a necessity. And you deserve to afford it.

Comments

Rob Deneke January 16, 2026 at 00:10

I used to pay $300 for my insulin until I found a 340B pharmacy down the street. Now it's $25. No coupon. No drama. Just walk in. You don't need to be a genius to save money if you know where to look.

Stop letting the system tell you it's impossible.

Henry Ip January 16, 2026 at 23:34

Generics are the real MVP here. My dad switched from Lipitor to atorvastatin and saved $200 a month. Same pill. Same results. Doctors don't always push it because they're not the ones paying. But you are. So ask. Always ask.

Kasey Summerer January 17, 2026 at 04:12

Oh wow a 40% discount on meds? Guess I'll just wait for the government to fix capitalism for me 🙃

Meanwhile my rent went up 30% and my pills are still $500. Thanks Obama.

kanchan tiwari January 17, 2026 at 13:36

THEY KNOW WHAT THEY'RE DOING. THIS ISN'T ABOUT COST. IT'S ABOUT CONTROL. THEY WANT YOU SICK. THEY WANT YOU DEPENDENT. THEY WANT YOU PAYING $500 FOR A PILLS THAT COSTS 12 CENTS TO MAKE. THE PHARMA COMPANIES OWN THE FDA. THE PBMS ARE THEIR LITTLE PUPPETS. AND YOU? YOU'RE JUST A CASH COW.

WHEN WILL WE WAKE UP?

Ryan Hutchison January 19, 2026 at 08:26

This whole thing is why America is still the best. We pay more because we innovate more. You think Canada's cheap insulin is because they're smarter? No. They're just free-riders. We fund the R&D. They copy it. Then they act like they're heroes for having cheaper prices. Wake up. This isn't greed. It's progress.

Samyak Shertok January 20, 2026 at 18:20

You think the system is broken? Nah. It's working exactly as designed. Capitalism doesn't care if you live or die. It only cares if you pay. The coupon? A distraction. The generic? A loophole. The prior auth? A ritual to remind you who's in charge. We're not patients. We're consumers. And consumers are always last on the list.

brooke wright January 21, 2026 at 02:33

I had to choose between my blood pressure meds and my kid's school trip last month. I picked the trip. I'm fine. He's fine. But I cried for an hour after. No one talks about this. Not even the doctors. They just hand you the script like it's a coupon for a free coffee.

vivek kumar January 22, 2026 at 18:26

The FDA's bioequivalence standards for generics are rigorous and scientifically valid. Multiple meta-analyses confirm no clinically significant difference in efficacy or safety between generics and brand-name drugs. The perception of inferiority is a marketing artifact, not a pharmacological reality. You are not being cheated by generics. You are being exploited by brand-name pricing.

Riya Katyal January 24, 2026 at 15:59

Oh so now we're supposed to trust GoodRx? Like that's not just another middleman selling our data to the same pharma companies who made the prices so high in the first place? Classic. We're all just pawns in a game where the board was never meant for us.

waneta rozwan January 25, 2026 at 22:38

If you're still taking brand-name drugs without asking for a generic, you're literally throwing money away. And if you're using coupons without checking the cash price? You're being scammed. This isn't hard. Stop making excuses. Your health isn't a luxury. It's your responsibility.

Nicholas Gabriel January 27, 2026 at 18:18

Please, please, please-ask your pharmacist if your pill can be split! I split my 20mg metoprolol into two 10mg doses and cut my cost in half. It's safe for most pills (check with your doc first), and no one ever tells you this. Also, NeedyMeds saved my life last year. I was so scared to apply… but it was easy. Just fill out the form. Don't let pride cost you your health.

swarnima singh January 28, 2026 at 05:57

i just want to live. why is that too much to ask? i take 5 pills a day. each one is a battle. i cry every time i open the bottle. i hate that i have to beg for medicine like it's charity. and now they want me to 'shop around' like i'm buying shoes? i'm not shopping. i'm surviving.

Isabella Reid January 29, 2026 at 12:22

I work in a community clinic. We see this every day. People skipping doses. Cutting pills in half with scissors. Some even sharing meds with family. It’s not just about money-it’s about dignity. The fact that we’ve normalized this is the real tragedy.

Jody Fahrenkrug January 29, 2026 at 12:39

I used GoodRx for my antidepressant and saved $120. Didn't even need to call my doctor. Just showed the receipt to my pharmacist and they matched it. So easy. Why didn't I know this sooner?

Allen Davidson January 30, 2026 at 22:58

I used to be one of those people who thought generics were 'weaker.' Then my wife got diagnosed with hypertension. We switched to lisinopril. Same effect. Same side effects. $4 instead of $120. I'm not a doctor. But I'm a husband. And I'm not letting her die because I was too proud to ask.